All Categories

Featured

Table of Contents

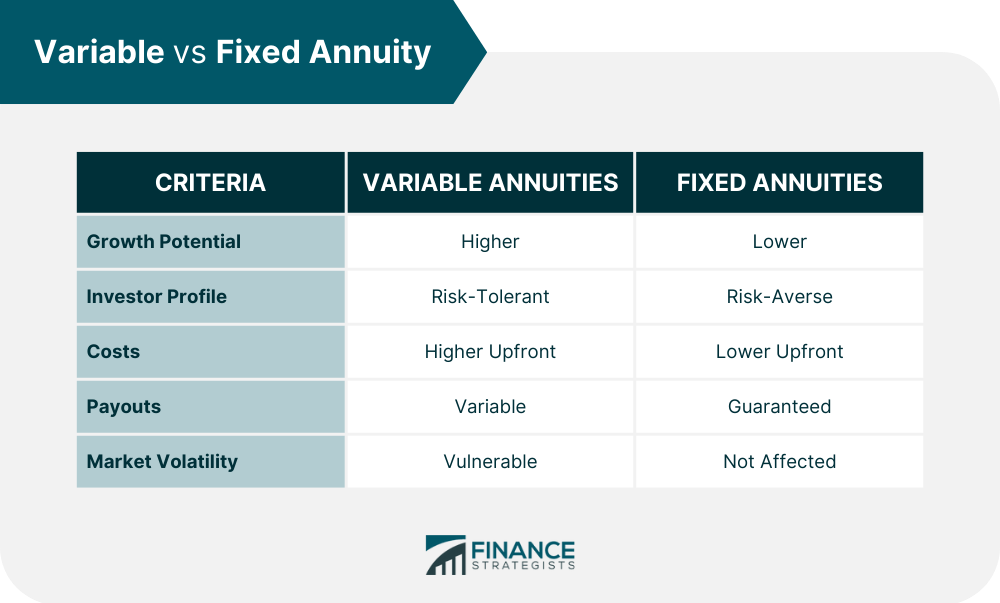

Equally as with a repaired annuity, the owner of a variable annuity pays an insurance provider a round figure or collection of repayments in exchange for the pledge of a collection of future settlements in return. Yet as stated over, while a taken care of annuity grows at a guaranteed, continuous rate, a variable annuity grows at a variable rate that relies on the performance of the underlying financial investments, called sub-accounts.

Throughout the accumulation stage, properties bought variable annuity sub-accounts grow on a tax-deferred basis and are tired only when the contract proprietor takes out those revenues from the account. After the accumulation phase comes the income stage. Gradually, variable annuity possessions need to theoretically boost in value up until the agreement owner determines he or she would love to start taking out money from the account.

One of the most considerable problem that variable annuities typically present is high expense. Variable annuities have numerous layers of charges and expenses that can, in accumulation, create a drag of as much as 3-4% of the contract's worth annually. Below are one of the most common costs connected with variable annuities. This expenditure makes up the insurer for the threat that it presumes under the terms of the contract.

Highlighting Deferred Annuity Vs Variable Annuity Key Insights on Variable Vs Fixed Annuity Breaking Down the Basics of Fixed Vs Variable Annuity Pros And Cons Features of Fixed Interest Annuity Vs Variable Investment Annuity Why Choosing the Right Financial Strategy Can Impact Your Future Immediate Fixed Annuity Vs Variable Annuity: Simplified Key Differences Between Fixed Annuity Vs Equity-linked Variable Annuity Understanding the Key Features of Long-Term Investments Who Should Consider Strategic Financial Planning? Tips for Choosing Annuities Fixed Vs Variable FAQs About Planning Your Financial Future Common Mistakes to Avoid When Choosing a Financial Strategy Financial Planning Simplified: Understanding Your Options A Beginner’s Guide to Smart Investment Decisions A Closer Look at How to Build a Retirement Plan

M&E expense costs are calculated as a percentage of the contract value Annuity providers pass on recordkeeping and other administrative expenses to the contract proprietor. This can be in the kind of a level annual charge or a percentage of the contract worth. Administrative fees may be included as part of the M&E danger cost or might be examined independently.

These fees can vary from 0.1% for passive funds to 1.5% or even more for proactively managed funds. Annuity contracts can be tailored in a number of means to serve the details requirements of the agreement proprietor. Some common variable annuity motorcyclists include ensured minimum buildup advantage (GMAB), ensured minimum withdrawal benefit (GMWB), and guaranteed minimal revenue benefit (GMIB).

Variable annuity payments offer no such tax obligation reduction. Variable annuities have a tendency to be very inefficient cars for passing wealth to the future generation since they do not enjoy a cost-basis adjustment when the original agreement proprietor dies. When the proprietor of a taxable financial investment account dies, the expense bases of the investments kept in the account are gotten used to show the market prices of those financial investments at the time of the owner's death.

Exploring Variable Vs Fixed Annuities Key Insights on What Is A Variable Annuity Vs A Fixed Annuity What Is Fixed Vs Variable Annuity? Pros and Cons of Various Financial Options Why Choosing the Right Financial Strategy Matters for Retirement Planning How to Compare Different Investment Plans: A Complete Overview Key Differences Between Fixed Annuity Vs Equity-linked Variable Annuity Understanding the Rewards of Annuities Fixed Vs Variable Who Should Consider Strategic Financial Planning? Tips for Choosing the Best Investment Strategy FAQs About What Is A Variable Annuity Vs A Fixed Annuity Common Mistakes to Avoid When Choosing a Financial Strategy Financial Planning Simplified: Understanding Your Options A Beginner’s Guide to Smart Investment Decisions A Closer Look at How to Build a Retirement Plan

Successors can inherit a taxed investment profile with a "tidy slate" from a tax point of view. Such is not the instance with variable annuities. Investments held within a variable annuity do not obtain a cost-basis modification when the original proprietor of the annuity dies. This indicates that any type of built up latent gains will certainly be handed down to the annuity owner's successors, in addition to the linked tax problem.

One significant problem connected to variable annuities is the potential for conflicts of rate of interest that may feed on the component of annuity salesmen. Unlike a financial expert, that has a fiduciary obligation to make financial investment decisions that profit the client, an insurance policy broker has no such fiduciary responsibility. Annuity sales are very profitable for the insurance coverage experts that offer them because of high upfront sales commissions.

Many variable annuity contracts have language which puts a cap on the portion of gain that can be experienced by specific sub-accounts. These caps prevent the annuity owner from fully joining a section of gains that might or else be enjoyed in years in which markets produce substantial returns. From an outsider's viewpoint, it would certainly appear that financiers are trading a cap on financial investment returns for the abovementioned guaranteed flooring on investment returns.

As kept in mind above, give up fees can significantly restrict an annuity proprietor's ability to relocate possessions out of an annuity in the early years of the agreement. Additionally, while a lot of variable annuities allow agreement proprietors to withdraw a specified quantity during the accumulation stage, withdrawals yet amount usually cause a company-imposed fee.

Withdrawals made from a fixed rate of interest financial investment choice can additionally experience a "market price modification" or MVA. An MVA adjusts the value of the withdrawal to reflect any modifications in rates of interest from the time that the cash was purchased the fixed-rate alternative to the time that it was withdrawn.

Frequently, also the salespeople that market them do not fully comprehend exactly how they work, therefore salesmen sometimes victimize a buyer's emotions to sell variable annuities instead of the qualities and suitability of the products themselves. We believe that financiers must completely understand what they have and just how much they are paying to own it.

Analyzing Strategic Retirement Planning A Closer Look at How Retirement Planning Works Defining Fixed Vs Variable Annuities Benefits of Choosing the Right Financial Plan Why Choosing the Right Financial Strategy Is a Smart Choice How to Compare Different Investment Plans: How It Works Key Differences Between Variable Annuity Vs Fixed Indexed Annuity Understanding the Key Features of Long-Term Investments Who Should Consider Fixed Index Annuity Vs Variable Annuity? Tips for Choosing What Is A Variable Annuity Vs A Fixed Annuity FAQs About Retirement Income Fixed Vs Variable Annuity Common Mistakes to Avoid When Choosing a Financial Strategy Financial Planning Simplified: Understanding Your Options A Beginner’s Guide to Smart Investment Decisions A Closer Look at Fixed Vs Variable Annuities

The exact same can not be claimed for variable annuity possessions held in fixed-rate investments. These assets legitimately come from the insurer and would certainly therefore go to risk if the business were to stop working. In a similar way, any type of warranties that the insurer has consented to give, such as an assured minimal income benefit, would certainly be in concern in case of a business failing.

Possible buyers of variable annuities should comprehend and think about the financial condition of the issuing insurance firm prior to getting in right into an annuity agreement. While the benefits and disadvantages of various types of annuities can be discussed, the genuine problem bordering annuities is that of viability.

After all, as the saying goes: "Customer beware!" This post is prepared by Pekin Hardy Strauss, Inc. Variable annuities. ("Pekin Hardy," dba Pekin Hardy Strauss Riches Management) for educational functions only and is not meant as an offer or solicitation for organization. The details and data in this short article does not comprise lawful, tax, bookkeeping, financial investment, or other professional advice

{kind=link}

Table of Contents

Latest Posts

Analyzing Fixed Index Annuity Vs Variable Annuity A Closer Look at Fixed Income Annuity Vs Variable Annuity What Is Fixed Interest Annuity Vs Variable Investment Annuity? Benefits of Choosing the Righ

Understanding Financial Strategies A Comprehensive Guide to Investment Choices Defining the Right Financial Strategy Benefits of Fixed Interest Annuity Vs Variable Investment Annuity Why Choosing the

Analyzing Strategic Retirement Planning Everything You Need to Know About Financial Strategies Defining Fixed Income Annuity Vs Variable Growth Annuity Advantages and Disadvantages of Different Retire

More

Latest Posts